|

Five Economic Storms Raging NOW!

by Martin

D. Weiss, Ph.D.

Dear Subscriber,

Any economist fixated on

so-called "signs of a recovery" needs to have his head examined.

As I'll prove to you in a moment,

the hard-nosed reality is that five major economic cyclones are in

progress at this very moment.

The storms are not abating. Nor

are they changing direction. Quite the contrary, what you see today is,

at best, merely a deceptive calm before the next, even larger tempests.

For investors who follow Wall

Street, it could be fatal.

For contrarian investors,

however, this insanity opens up some of the greatest opportunities in

many years: Precisely when we see plunging barometers all around us, we

also have a new surge of hype on Wall Street, driving stock prices

higher.

Result: The rally has lowered the

cost of contrary investments precisely when their prospects are best.

Consider the five storms, and you'll see exactly what I mean ...

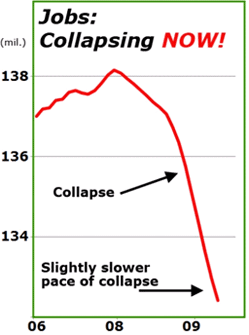

Storm

#1.

Plunging

Jobs

On Friday, the Bureau of Labor

Statistics announced that job losses were running at a slightly slower

pace than in the first quarter. So Wall Street cheered.

But it's a joke, and the 539,000

additional Americans out of work aren't laughing.

Nor are the 23 million people �

15.8 percent of the work force � who are officially unemployed ... are

struggling with lower paying part-time jobs ... or have given up

looking for work entirely.

Look. In December 2007, there

were 138.1 million jobs in America. Now, there are only 132.4 million.

So even if you accept the

government's tally of the narrowest unemployment measure, 5.7 million

jobs have been lost.

Plot those figures on a chart and

the picture is absolutely unambiguous: Jobs in America are collapsing.

Right here and now!

Where's that "slightly slower

pace of collapse" they're raving about? You'd need a microscope to see

it.

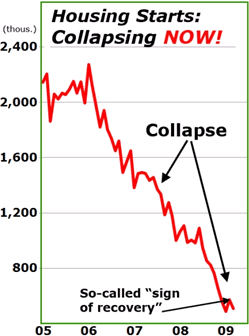

Storm

#2

U.S.

Housing Starts Down 77.6 Percent!

Housing is the nation's largest

industry. With it, the entire global economy boomed in the mid-2000s.

Without it, a recovery is next to impossible.

The big picture: Housing starts,

the best measure of the industry's health, peaked at an annual pace of

2.3 million units in early 2006.

Now, they're running at barely

more than a 0.5 million units.

That's a decline of 77.6

percent � three-quarters of America's largest single industry wiped

out.

Yes, back in February, there was

a tiny uptick: Starts rose from 488,000 to 572,000. And everywhere we

heard voices cheering the "spectacular" jump in housing starts.

What they didn't tell you is that

the so-called "jump" was actually smaller than six of the seven minor

upticks we've seen in housing starts since 2006. Nor did you hear them

say much when this measure fell anew in March.

Subscriber, this industry is not recovering. It remains in a

state of near total collapse.

The only major change: Lenders

have given up waiting for a recovery that never comes. So they're

throwing in the towel, unloading huge inventories of foreclosed

properties at fire-sale prices. And they're calling that a "recovery"?

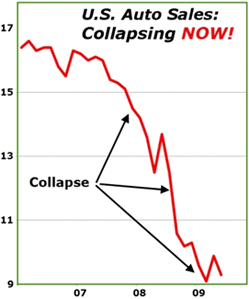

Storm

#3

Auto Sales Down 44

Percent!

At their peak in February 2007,

U.S. and foreign-owned companies sold automobiles in America at an

annual pace of 16.6 million units.

Last month, their sales pace

plunged to 9.3 million, a decline of

44 percent (including the best performers like Toyota and Honda).

Again, as with housing, we saw a

tiny uptick in the prior month, hailed by high officials as a "sign" of

improvement. Yet, as with housing, it was weaker than all prior "signs

of a turn" over the past 26 months � each of which was followed by a

sharper plunge.

Any lights at the end to

Detroit's dark tunnel? Only those of three speeding freight trains:

-

The Chrysler bankruptcy, despite all the talk of a

"quick and easy" procedure, is not only frightening U.S. car buyers

away from the Chrysler brand, it's also scaring them from other U.S.

and foreign makers. And it's not only hurting auto dealers and parts

suppliers, but also smacking auto lenders. Meanwhile ...

-

GMAC, the nation's largest auto

lender, is already in its death throes, with the government now

estimating it could suffer additional losses of a whopping $9.2 billion

over the next two years. Will the Obama administration bail it out?

Perhaps. But it would still have to downsize its operations, throwing

another monkey wrench into General Motors' sales. Meanwhile ...

-

General Motors is now sinking even more rapidly

toward bankruptcy than it was just a few months ago. According to last

week's New

York Times

column, G.M.,

Leaking Cash, Faces Bigger Chance of Bankruptcy ...

"Even after receiving $15.4

billion in federal loans, General

Motors is once again on the brink of

financial collapse.

"The automaker's first-quarter

earnings released Thursday showed that G.M. was losing more money and sales

than it was in late December, when the government began its bailout.

"With its cash reserves down to

the bare minimum and its revenue plunging, G.M. seems more certain each

day to be heading toward a bankruptcy filing. ...

"The company's chief financial

officer, Ray Young, called the drop ... 'a staggering number,' and said

consumers were showing increasing concern about G.M. products because

of the potential for bankruptcy."

General Motors' CFO added: "Once

you start losing revenues, you get yourself into a vicious cycle from

which you cannot recover."

Sound familiar? It should. It's

the same vicious cycle I've been warning about for many moons � falling

revenues prompting mass layoffs, and mass layoffs driving down

revenues.

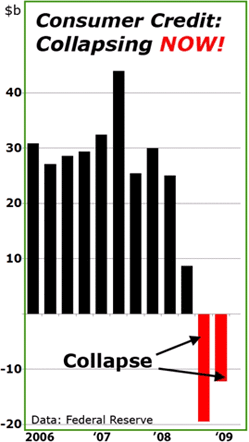

Storm

#4

Biggest

Decline in Consumer

Credit Ever Recorded!

Any economist counting on the

consumer to get things going again had better go back for some more

Rorschach tests ...

... because you don't need a

therapist to interpret the image depicted in my chart below. It shows

very clearly how the nation's lenders are dumping consumers and making

a mad dash for the exits:

In the third quarter of 2007,

banks dished out $44 billion in net new loans on credit cards, autos,

and other consumer credit (excluding mortgages).

Then, just 12 months later, in

the third quarter of 2008, that giant credit machine collapsed to a

meager $8.7 billion, a

decline of 80 percent!

But the collapse didn't end

there. In last year's fourth quarter, not only did new credit

disappear, but lenders actually pulled out of the consumer credit market to

the tune of $19.5 billion.

And they did it AGAIN in the

first quarter of this year, pulling out another $12.2 billion.

It is the biggest

collapse in consumer credit ever recorded.

Now do you see why I'm

recommending a shrink for any economist fixated on a recovery?

They know how important credit

is. They know that few Americans have the savings to splurge on

consumer goods. And they're tired of knowing that a recovery is

virtually impossible without credit.

And yet here we are, with the

biggest-ever collapse in consumer credit � and they're still searching for the "signs"!

Storm

#5

Big

Banks!

Whether the government lets big

banks fail or not, the impact on the economy is similar: A massive

contraction of bank loans and credit, sabotaging attempts to revive

credit flows and stimulate the economy.

Reason: These banks must build

capital quickly, and the only realistic way to do so is by cutting back

on their lending.

The official stress test results

released Thursday on 19 U.S. bank holding companies were supposed to

help determine exactly how much capital they'll need, and the total

came to $75 billion.

That's no small amount. But the

stress tests will go down in history as the world's most elaborate

effort to paint lipstick on a pig.

To show you why, first, let me

provide our analysis based on data from TheStreet.com Ratings, the

Comptroller of the Currency (OCC), and the banks' first-quarter

financial statements. Then I'll show you why I believe the official

results grossly underestimate how much capital the banks will need and

how much pressure they'll be under to slash lending.

We find that ...

-

Seven institutions � JPMorgan

Chase & Co., Citigroup, Wells Fargo & Co., Goldman

Sachs Group, GMAC LLC, SunTrust Banks, Inc., and Fifth Third Bancorp �

are at risk of failure and may have to cut back lending dramatically to

stay alive.

-

Eight institutions � Bank of

America, Morgan Stanley, PNC Financial Services Group, US Bancorp,

BB&T Corp., Regions Financial Corp., American Express Co., and

Keycorp � are borderline, meaning they could be at risk of failure with

worsening economic or financial conditions and will also have to cut

back on lending.

-

Only four institutions � MetLife,

Bank of NY Mellon Corp., Capital One Financial Corp., and State Street

Corp. � appear to have adequate capital to withstand worsening

conditions. But even they may voluntarily cut back their lending in an

attempt to maintain their current financial health.

Moreover, of the $11.6 trillion

in assets held by the 19 institutions, those likely to cut back

dramatically represent $6.56 trillion, or 56.5 percent, of the assets;

while borderline institutions hold $4 trillion, or 34.7 percent.

Only $1 trillion � just

8.8 percent � of the assets are held by institutions with adequate

capital, based on our analysis.

In contrast, the government is

trying to persuade us that most have plenty of capital ... the rest can

easily raise it ... and none will have to slash lending in a

way that would sabotage the prospects for an economic recovery.

So what explains this vast

discrepancy between the official conclusions and ours?

The simple answer: Three

unmistakable deceptions in the government's stress tests ...

First deception: The

assumptions.

To come up with estimates of

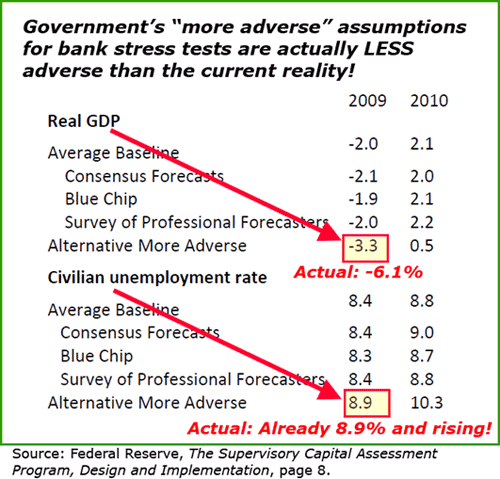

future losses, the government assumed what they call "a more adverse"

scenario. But their more adverse scenario is actually less adverse than the current

reality!

Hard to believe? Then just look

at their own numbers in the chart the Fed published recently:

-

Their "more adverse" scenario is

predicated on the presumption that the GDP will contract no more than

3.3 percent this year. But in actuality, the GDP is already contracting at an annual pace of

6.1 percent!

-

Their "more adverse" scenario

also assumes that unemployment will average 8.9 percent this year. But

unemployment has already reached 8.9 percent in April,

and no one � not even economists fixated on recovery signs � is

anticipating anything but a further rise.

Either they're delusional. Or

they're cheating at solitaire.

Second deception: No

mention of systemic risk!

The banking regulators have

published two major white papers on the stress tests � "Design

and Implementation" plus "Overview

of Results." However, in these papers, they have failed to

even mention the greatest risk of all: systemic risk.

This is the risk that ...

-

A few key players in highly

leveraged instruments like derivatives could default on their trades.

-

These defaults could set off a

series of failures, with the most severe impacts felt by banks that

hold the largest share of the derivatives in the country.

This is the giant risk that the

Government Accountability Office (GAO) wrote about in its landmark 1994

study, "Financial

Derivatives: Actions Needed to Protect the Financial System," warning of "a chain reaction

of market withdrawals, possible firm failures, and a systemic crisis."

This is the giant risk that

triggered the collapse of Bear Sterns, the failure of Lehman Brothers,

and the $180 billion bailout of America's largest insurer, AIG.

It's the giant risk that AIG

executives themselves wrote about in their recent memorandum, "AIG:

Is The Risk Systemic?," warning of a "cascading impact

on a number of life insurers already weakened by credit losses" ... and

"a chain reaction of enormous proportion."

It's the giant risk that the

International Monetary Fund is most concerned about when it warns of

another $3 trillion in global losses due to the banking crisis.

It's the giant risk that prompted

former Treasury Secretary Henry Paulson to literally drop to his knees

last September, begging Congress for $700 billion in bailout funds for

the banking industry.

Since that day, the U.S. economy

has suffered the worst back-to-back GDP declines in over 50 years,

burning the nation's fuse even closer to a blow-up.

And yet, suddenly, in a massive

undertaking that was supposed to accurately evaluate the banks'

exposure to these dangers, it's also the giant risk that has been

scrupulously scrubbed from 59 pages of official white papers, a half

dozen press releases, plus multiple public pronouncements � all about

the stress tests, all without a single mention of systemic risk.

This omission is both deliberate

and unforgivable.

It means the stress tests have

failed to fairly evaluate the credit exposure of each bank to defaults

by their trading partners. And it means the tests are creating a false

sense of security for investors and the public that can only lead to

greater mistrust, more loss of confidence, even panic.

The omission is especially

misleading for large banks that dominate the derivatives market ...

would be at ground zero in any meltdown ... and would therefore be

among the first to suffer massive losses.

The prime example: The OCC

reports that, at year-end 2008, JPMorgan Chase (JPM) held $87.4

trillion in notional value derivatives, including $8.4 trillion in

credit default swaps.

(To see for yourself, click

here to download the OCC's latest

report; scroll down to page 22; and check out the top line "JPMorgan

Chase Bank NA." Note: The next to the last column "Total Credit

Derivatives" is 99 percent made up of credit default swaps, according

to the OCC.)

Why is this such a big problem?

For several reasons:

-

Although it's cut back a bit, JPM

still has 43.6 percent of all the derivatives held by all U.S.

commercial banks, or $17 trillion more than Bank of America and

Citibank combined. Among the 19 bank holding

companies in the stress tests, that puts JPM closer to ground zero than

any other bank.

-

It's well known that credit

default swaps are the highest-risk sector of the derivatives market.

And yet, in this sector, JPM has 52.8 percent of the total held by all U.S.

commercial banks, or nearly double the total held by BofA and Citi.

This puts JPM even closer to ground zero.

-

JPM execs insist they're smart

and know how to handle their risks very neatly. But if that were the

case, why did they suffer a whopping $2.5 billion loss in their credit

default swaps in the fourth quarter? (OCC, page 27, Table 7, line 1, last

column.)

-

The OCC also reports that, for

each dollar of capital, JPM still has $3.82 in total credit exposure.

Mind you, that's JPM's exposure to just one kind of risk (defaults by

trading partners) in just one kind of instrument

(derivatives). In addition, JPM is also assuming market risks in derivatives plus a

series of risks in its other investing and lending operations. (OCC, page 13, table at bottom of

page, line 1, last column.)

-

Despite all this, in their "more

adverse" scenario, the banking regulators estimate JPMorgan Chase's

total "counterparty and trading losses" will not exceed $16.7 billion,

a fraction of the true potential losses in a financial crisis.

With the fatal omission of

systemic risk from their analysis, the government concludes that

JPMorgan Chase is in good shape and does not need any additional

capital.

The same omission leads to a

similar conclusion for Goldman Sachs, despite the fact that Goldman has

over $10 in total credit exposure per dollar of capital, or nearly

triple the credit risk of JPMorgan Chase.

The only realistic conclusion:

Both these institutions will need huge amounts of capital, driving them

to cut back massively on new lending.

Systemic risk is the

elephant in the room. Everyone knows it's there.

Everyone understands the dangers. But they're afraid of the answers. So

they dare not ask the questions.

The fundamental answer, though,

is clear: Systemic risk is what drove the financial markets into a deep

freeze seven months ago; and it was that storm which helped drive the

economy into a tailspin.

Today, systemic risk is not gone.

If anything, it's far worse.

Third Deception:

Improper influence.

In its white paper, the Federal

Reserve admits that the stress tests were based, to a large extent, on

each bank's self-evaluation � not only for loan loss estimates that can

be derived from past data, but also for the future performance of

trading accounts, which can be far more subjective.

Moreover, each institution was

allowed to appeal the final results, and several banks strenuously

negotiated for more favorable grades. They even got regulators to

accept their projections of future revenues, treating those future

revenues almost as if they were cash in the kitty.

In contrast, we never permit the

companies we evaluate to influence our evaluation process or our

results. To do so would defeat the entire purpose of the exercise. But

much like conflicted Wall Street rating agencies, that's essentially

what the bank regulators have done � from start to finish.

Put simply, the stress tests were

too easy; the banks took the exams home with cheat sheets; and if they

didn't like their final grade, they could get the examiners to give

them a better one.

Yet despite all these fudge

factors, the government still estimates these institutions could suffer

$600 billion in additional losses over the next two years.

And this is being portrayed as

another "sign" of recovery?!

My view: We will have a recovery someday. But

only AFTER we honestly recognize the grave mistakes of the past and own

up to the hard sacrifices still ahead.

Until that happens, I'm staying

the course, investing my own money in a way that protects me from the

dangers and gives me an opportunity to profit from the next decline ...

which, by the way, promises to be the biggest of all.

If you want to follow along with

me, check your inbox for an alert that I'll soon be sending you

personally � with the sender name "Martin D. Weiss, Ph.D."

Good luck and God bless!

Martin

About

Money

and Markets

For

more information and archived issues, visit http://www.moneyandmarkets.com

Money

and Markets (MaM) is

published by Weiss Research, Inc. and written by Martin D. Weiss along

with Tony Sagami, Nilus Mattive, Sean Brodrick, Larry Edelson, Michael

Larson and Bryan Rich. To avoid conflicts of interest, Weiss Research

and its staff do not hold positions in companies recommended in MaM, nor

do we accept any compensation for such recommendations. The comments,

graphs, forecasts, and indices published in MaM are

based upon data whose accuracy is deemed reliable but not guaranteed.

Performance returns cited are derived from our best estimates but must

be considered hypothetical in as much as we do not track the actual

prices investors pay or receive. Regular contributors and staff include

Kristen Adams, Andrea Baumwald, John Burke, Amber Dakar, Dinesh Kalera,

Red Morgan, Maryellen Murphy, Jennifer Newman-Amos, Adam Shafer, Julie

Trudeau, Jill Umiker, Leslie Underwood and Michelle Zausnig.

Attention

editors and publishers! Money

and Markets

issues can be republished. Republished issues MUST include attribution

of the author(s) and the following short paragraph:

This

investment news is brought to you by Money

and Markets. Money

and Markets is a

free daily investment newsletter from Martin D. Weiss and Weiss

Research analysts offering the latest investing news and financial

insights for the stock market, including tips and advice on investing

in gold, energy and oil. Dr. Weiss is a leader in the fields of

investing, interest rates, financial safety and economic forecasting.

To view archives or subscribe, visit http://www.moneyandmarkets.com.

From

time to time, Money

and Markets may

have information from select third-party advertisers known as "external

sponsorships." We cannot guarantee the accuracy of these ads. In

addition, these ads do not necessarily express the viewpoints of Money

and Markets or

its editors. For more information, see our terms and conditions.

View

our Privacy Policy.

Would

you like to unsubscribe from our mailing list?

To

make sure you don't miss our urgent updates, add Weiss Research to your

address book. Just follow these simple steps.

|

� 2009 by Weiss Research, Inc. All rights

reserved.

|

15430 Endeavour Drive, Jupiter, FL 33478

|

|

Hopefully

and prayerfully the true people in God�s Church are not

refusing to see these terrible problems and should know from their

studies of their Bibles this country is soon to reap what it has

sown!

Hopefully

and prayerfully the true people in God�s Church are not

refusing to see these terrible problems and should know from their

studies of their Bibles this country is soon to reap what it has

sown!